In a world of economic uncertainty and rising costs, an effective budget is a safeguard from these risks. At Capital Compass, we view budgeting as more than just a spending tracker; it's a tool that provides stability and security, setting up young adults for financial success. Without one, it’s easy to fall into common traps: overspending, accruing high-interest debt, and feeling constant stress about money. We've seen people graduate with strong job prospects yet still live paycheck to paycheck, not because they don’t earn enough, but because they never learned how to manage what they earn. At Capital Compass, we believe budgeting is about freedom rather than restriction. Freedom to save for what matters, prepare for the unexpected, and build a foundation for long-term financial health. Our approach to budgeting emphasizes clear, simple, and adaptable methods from trusted sources and tools to help ensure that young adults control their money, rather than their money controlling them.

Budgeting can feel like trying to keep sand from slipping through your fingers—no matter how careful you are, it just disappears. The 50/30/20 rule is a simple yet powerful way to keep that sand (your money) in the right buckets. It’s not about spreadsheets with 50 categories or depriving yourself—it’s about creating a balanced plan you can actually stick to.Here’s how it works:

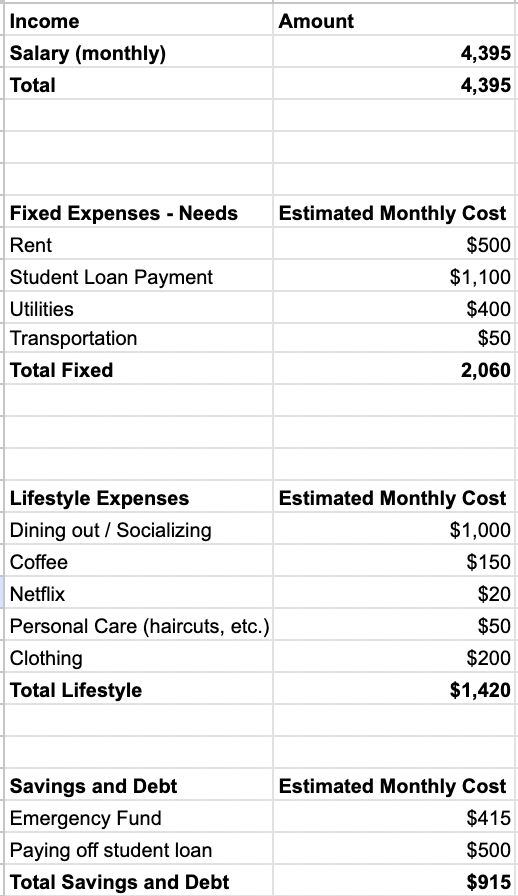

50% Needs – Half your take-home pay goes toward essentials: rent, groceries, utilities, transportation, insurance. These are the things you can’t cut without serious consequences.

30% Wants – About a third of your income funds the fun stuff: dinners out, Netflix, hobbies, vacations, that latte you look forward to every morning. Yes, this category exists so you don’t feel like budgeting is a financial prison.

20% Savings & Debt Repayment – The final chunk goes toward building your future: emergency funds, investments, retirement accounts, and extra payments on debt. This is your “future you” fund.

It’s simple enough to remember without pulling out a calculator every five minutes, but still structured enough to keep you accountable. Unlike ultra-restrictive budgets, it recognizes that spending on things you enjoy is important—if you cut out all fun, you’ll probably quit the budget within weeks.

Say you take home $3,000 a month after taxes. Under the 50/30/20 rule: $1,500 goes to needs (maybe $900 for rent, $300 for groceries, $150 for utilities, $150 for gas/transportation).

$900 goes to wants (could be $150 for eating out, $80 for streaming and subscriptions, $400 for travel savings, $270 for weekend activities).

$600 goes to savings/debt (maybe $300 to an emergency fund and $300 to retirement)

The key is to be realistic. If your rent alone eats up 60% of your income, the rest of your budget will feel impossible—you may need to adjust categories or find ways to cut fixed costs. Another tip: automate your savings. If $600 leaves your checking account the moment your paycheck lands, you’re less likely to “accidentally” spend it. Budgeting isn’t about perfection—it’s about direction. The 50/30/20 rule gives you a simple compass to follow so your money consistently supports your needs, your wants, and your future.

**The content on Capital Compass is for educational purposes only and does not constitute financial, legal, or investment advice. We are not financial advisors. Links to third-party sites are provided for convenience and do not imply endorsement. Always consult a qualified professional before making financial decisions.